China, the world’s largest vehicle market, recently announced that they are working towards banning the production and sale of petrol and diesel cars in the near future.

Britain and France also aim to ban all new petrol and diesel cars and vans from 2040 onwards. Increasingly, governments around the world are also jumping onto the “ban-wagon”, pushing the automotive industry towards electrification.

How Does This Affect PGM Demand and Supply?

PGM (platinum group metal) recyclers commonly collect catalytic converter from diesel and petrol vehicles, where PGMs can be found and extracted. These are usually a mix of Platinum, Palladium and Rhodium.

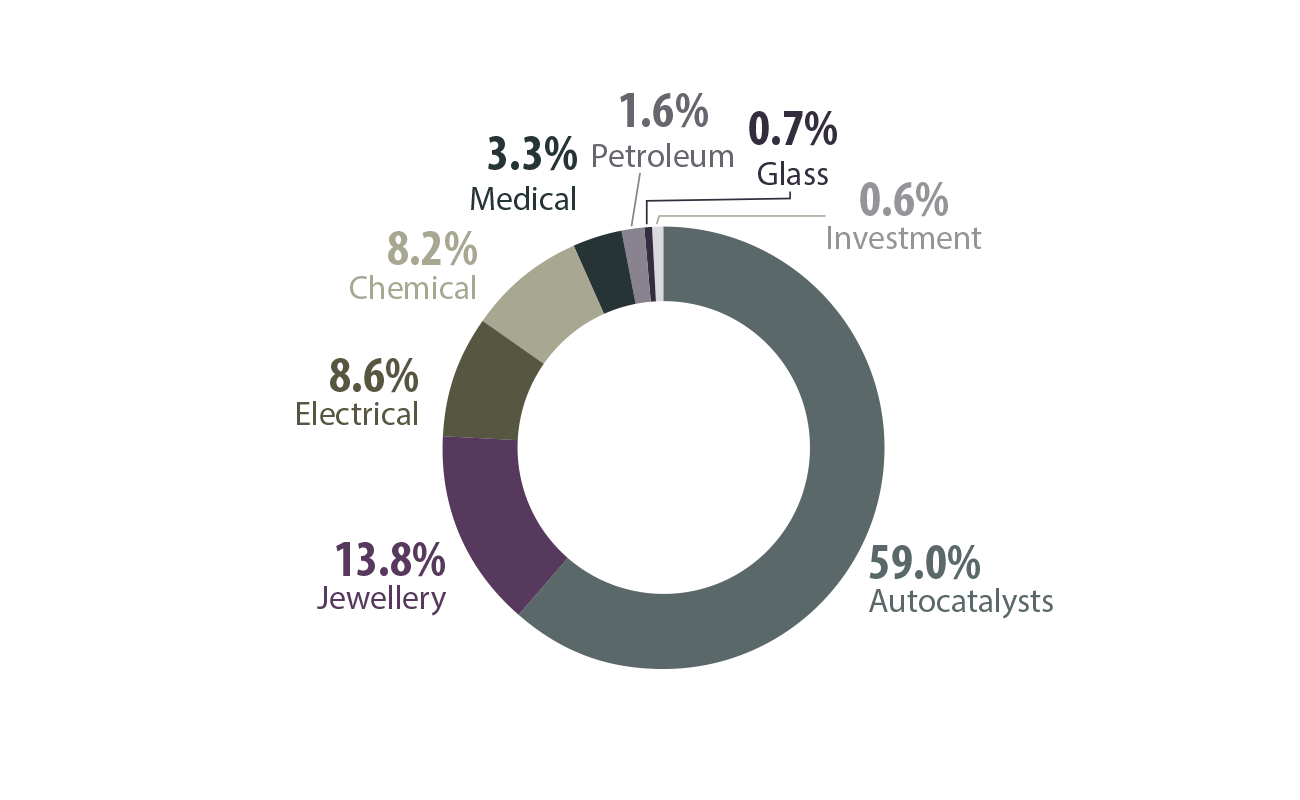

The largest demand for PGMs lies in the manufacturing of automotive catalytic converters, a whopping 59% of global PGM supply in 2016.

As EVs (electric vehicles) do not need converters, a ban on fossil fuel vehicles will cause PGM demand to drop significantly in the mid to long run.

PGM supply, however, is a different story altogether.

In 2016, the global vehicle population reached 1.32 billion cars and trucks and continues to grow year on year.

Even if fossil fuel vehicles were to be banned with immediate effect, that would leave us with an abundant supply of PGMs – more than a billion converters on the roads.

Given the way the market is heading, PGM demand looks set to weaken amidst rising supply. Unless the fall in PGM demand is offset by new applications like fuel cell, excess supply will exert downward pressure on PGM prices in the next 10 to 15 years.

How Will This Affect the PMG Recycling Industry?

PGM smelters need to process and sell large volumes of PGM in order to cover operating costs. A substantial drop in demand might force some refineries out of business.

This is similar to what aluminium smelters went through during the 2008 global financial crisis. Aluminium prices collapsed and inventory ballooned, forcing aluminium smelters to shut down like dominos.

At the end of the late 90’s, the United States had 22 aluminum smelters, only 8 remained by the end of 2015.

In the case of PGM smelters, the process will probably be more gradual, as the vehicle bans have been announced years ahead of time, allowing smelters to adjust to new market conditions.

Catalytic converter collectors, on the other hand will face a two-pronged problem.

Firstly, lower prices will mean collectors eventually have to collect and process a higher volume of catalytic converters for the same amount of returns. So be prepared to invest in new technologies that will enhance productivity whilst reducing operational and manpower costs.

Secondly, with the fall in demand, chances are the surviving refineries will stop extending favourable pre-payment terms to collectors. Hence, even if collectors managed to increase their collection volume, some might have difficulty ensuring sufficient cash flow to buy new supplies and meet other overheads. Nevertheless, these problems can be mitigated by planning ahead and building a strong revenue reserve while the good times still roll.

How Can Recyclers Prepare for the Future?

In light of these future developments, some recyclers have started to explore recycling other types of waste. Let’s look at three possible options for the mid to long-run.

Option 1 – E-Waste

E-waste contains a host of highly recyclable materials including platinum, gold, cobalt and copper.

Although E-waste recycling has been around for a while, global e-waste levels are still rising, as much as 63% over the last five years. In 2016 alone, 44.7 million metric tonnes of e-waste was generated – the equivalent of almost 4,500 Eiffel towers!

The growth in e-waste volumes is also bolstered by growing trends like the Internet of Things (IoT). It is projected that by 2020, the world will have 50 billion devices and machines talking to each other. This is a rich minefield of precious metals waiting to be extracted and returned to the supply chain.

However, recyclers can longer rely on low-cost processing in China as the new ban on e-waste imports into the country comes into effect. They will have to quickly look for an alternative, cost-effective recycling solutions outside of China to seize these emerging opportunities.

Option 2 – Battery Waste

As of 2016, the EV population reached 2 million but is still a negligible percentage of the global vehicle population. Even under a fast adoption scenario, it may take another 25 to 30 years before we can see a sizeable amount of EV waste.

What recyclers can do instead, is to start recycling materials that will eventually be used in EVs. This includes lithium, cobalt, nickel, manganese, and graphite, which will be used in EV batteries.

As EVs start to gain traction, it raises concerns on whether lithium and cobalt supplies can keep up with demand.

More than 60% of the world’s supply of cobalt comes from the DRC (Democratic Republic of Congo). Sourcing from the DRC runs the risk of controversy, due to their reputation for infringing on human rights in its cobalt production practices.

This supply constraint creates a demand for cobalt-recycling to supplement supply levels. Lithium also has untapped recycling potential. As of today, only less than 5% of old lithium batteries are being recycled.

Sources of lithium and cobalt include batteries that fail quality tests and are disposed of as well as used batteries. The former makes up 1 in 10 of all lithium-ion batteries produced, and the latter can add up to a sizeable volume. Recycling these batteries alone could yield as much as 4,000 tonnes of cobalt.

Lithium and cobalt can also be recycled from the billions of end-of-life smart devices disposed of each year. In them lies the potential to have enough lithium and cobalt to power millions of electric vehicles.

Option 3 – Fuel Cell Vehicles

A third option would be to recycle platinum from fuel-cells. This is a long-term strategy that would take place say, in the next 10 to 20 years but for now, there aren’t enough fuel-cell vehicles on the road to make it a viable business proposition.

Fuel-cell vehicles rely on a platinum fuel-cell to generate energy from hydrogen, emitting only water vapour and warm air. They are often touted as an alternative to electric vehicles in the zero-emissions arena.

Should fuel-cell vehicles take off in a big way, it will create a new stream of demand for platinum and platinum-recycling in the mid to long-term. Anglo American Platinum CEO Chris Griffith estimates that fuel cells will spur a 500,000 oz demand for platinum by 2025.

In the meantime, markets like China and Japan are already pushing for heavy duty fuel-cell vehicles. Germany also targets to build 400 hydrogen refuelling stations to by 2023 and California 500 by 2022. Japan already has 80 existing hydrogen stations. This makes driving fuel-cell vehicles a more viable option for consumers in the mid-term.

However, a few potential pitfalls surround the viability of fuel-cell recycling even in the long term.

Firstly, platinum is expensive. Manufacturers are hard-pressed to lower the platinum loading per vehicle in order to make it cost-effective for consumers.

Mercedes has managed to reduce their platinum loading by 90%, using 10 grams of platinum in their GLC F-Cell. Toyota, on the other hand, is working towards cutting their platinum loading by 50%.

Lower platinum loadings in fuel cells mean that the boom in platinum demand will not be as previously anticipated.

Secondly, we will need more countries to follow the lead of Germany, US and Japan in the building of hydrogen refuelling stations. If not, fuel-cell vehicles will be unable to achieve high adoption rates on a global scale.

Lastly, fuel-cell vehicles still have to contend for market share with the lower-priced EVs. However, they do have two distinct advantages – longer driving ranges that is similar to gasoline or diesel-only vehicles and fast refuelling.

If these challenges can be overcome, fuel-cell recycling will be a profitable proposition for first movers.

All in all, the market outlook is…

Although platinum currently has a slight boost in the jewellery and industrial sectors this year, vehicle electrification will definitely impact PGM demand and pricing negatively in the mid to long term.

Unless the platinum-laden fuel cell vehicle overtakes the conventional EV in market and mindshare, catalytic converter recyclers will have to find alternatives, weigh the options and adapt quickly to save themselves from a similar fate as some of the aluminium smelters that went down during the last global financial storm.

In conclusion, E-waste would be a safe bet, but both fuel-cell and battery waste recycling do present early-mover advantage for recyclers in spite of the pitfalls.

Are you a PGM recycler? Which option(s) will you pick? Or are you considering other options? We’d love to hear from you. Share your thoughts with us at info@brmetalsltd.com.

If this article was helpful or will be helpful to someone you know, feel free to click on the share buttons on your left. We’d be happy to know someone benefited from reading this.

See you at the next post 🙂

{kind=link}